Today, I have a great article from Neiko Johnson on how he and his wife Alexis paid off $240,000 in just 27 months. They share their finance knowledge and debt-free journey on their blog Secret to Finance. The primary focus of their blog talks about budgeting, paying off debt, and building generational wealth by investing.

My wife Alexis and I have been married since 2018 and both brought a lot of debt into our marriage. We thought we were living a normal life but quickly realized what we were doing wasn’t going to work in the long run.

Like most people, we got into a routine that could lead us down the wrong path of ending up broke. We were simply enjoying life and didn’t have a good financial plan to build wealth.

There’s not an easy path to wealth but in this article, I will outline the steps my wife and I took to pay off $240,000 in 27 months and create a path to wealth.

I hope our story inspires you to take action on your financial journey and teach you some helpful tips that we use.

Our Background – Who We Are and What We Do

We’re Neiko (33) and Alexis (31) from Atlanta, GA. Neiko was born and raised in Atlanta and Alexis was born in Miami and raised in Anchorage, Alaska. Neiko works in Cybersecurity and Alexis is a general dentist.

About 4 years ago we set a goal to both retire by the age of 50. So, to reach this goal we had to make some financial changes and focus on how to pay off debt and create passive income.

However, we first had to create a plan to get out of debt. It was not an easy process to change our entire life habits but we knew we had a bigger goal in mind. We were 100% committed to reaching our financial goal of being debt-free within 5 years.

We decided to learn everything we could about money including saving, getting out of debt, budgeting, and investing.

It has always been our goal to be wealthy so we can help others learn how to become wealthy also. With our blog, we now help others create a financial plan that focuses on achieving financial freedom.

Why We Got Started and What Kept Us Motivated

Learning how to build wealth has become a very common topic in today’s society. I view being rich and wealthy as 2 different things.

Being rich simply means spending a lot of money regardless if the person has the money or not.

On the other hand, being wealthy is when you make smart money moves and have a plan for your finances. I call this “truly rich.”

We got started on our financial journey because we want to be “truly rich”, change our family tree, and live with financial freedom. The day we realized that we had a responsibility to manage our money the right way, we completely changed our approach.

We strongly believe everyone deserves to live with financial freedom and these principles helped change our financial perspective:

Living on a budget is important and is the key foundational aspect that is needed.

Paying off debt as soon as possible and not adding anymore debt will help you reach financial freedom faster.

To build wealth it’s important to save money and live on less than you make.

Investing as early and often as possible will allow you to retire on time and possibly early.

Reaching a financial goal takes sacrifice. However, the sacrifice is temporary. The day we decided to go all-in on changing our lifestyle so we can pay off debt and put more money in our pocket, it required a mindset shift.

Having something that reminds us of what we’re working towards will keep us focused on the ultimate goal. Our trust in each other and learning the right financial principles have been key aspects during our journey. Living with purpose is a big reason why we are so determined to reach our financial goals.

Having a purpose has allowed us to think clearer, make better financial decisions, and pay closer attention to the things we spend time doing each day.

Getting out of debt will allow us to have more money to invest, retire early, and enjoy life. This mentality keeps us motivated to continue on our financial journey even when times get hard.

As everyone is aware, the events of 2019-2021 required all of us to make adjustments in our lives. It became apparent that financial security is even more important when an emergency happens.

People lost their jobs and income and weren’t sure how they would pay bills or put food on the table.

That’s not a great feeling.

Reaching financial freedom is the main goal and takes hard work. But, every day we wake up we know we are working towards something great. We don’t want to have to worry about anything when the next financial crisis happens. It’s our goal to be financially secure where we don’t experience any setbacks if things seem shaky in the world.

Fortunately, during this time period we both were still employed and didn’t lose any income. However, it was another wake-up call for us to start focusing on creating additional streams of income just in case one stream of income is impacted unexpectedly.

So, we have started preparing ourselves to increase our investment portfolio. Currently, we only invest in our employer’s 401(k) but have plans to start investing in real estate and a dental business. This will allow us to increase our income to build generational wealth.

The way we have started learning real estate is by taking the course Make Real Estate Real. This course has given us the foundational knowledge needed to get started in real estate with the right strategies.

Educating ourselves is the key to increasing our income. It won’t happen overnight but we are taking baby steps to add more streams of income.

A wealth mindset understands that investing is a long-term play. You have to be on a budget, pay off debt, and save so you can invest in your future without restrictions.

How Much Debt Did We Start With and What Types?

Before we get into how we paid off debt so fast, I want to give a little background on how we got into so much debt, to begin with.

I think it’s important to provide transparency on where we started and where we are now. I believe readers need to understand that we didn’t just flip a light switch and suddenly pay off debt fast.

We were not managing money correctly and it was obvious due to the amount of debt we accumulated. Many nights we look back on how much progress we’ve made and it’s an amazing journey to reflect on.

We were terrified when we had $460,000 of debt in 2018.

Our debt included:

Student loans

Car loans

Credit cards

Medical loans

Personal loans

Being newlyweds with this amount of debt created frustration at times. But, at the time we didn’t think anything of it because most people had debt and we thought it was normal.

Alexis and I both have graduate degrees and that was very expensive, to say the least. The bulk of our debt came from dental loans when Alexis attended Tufts University in Boston. It’s very hard to cashflow dental school and most dentists graduate with $350,000 of debt and sometimes more.

However, Alexis was very intentional before attending dental school and secured some scholarships to limit the number of loans she needed. She graduated with around $225,000 of dental loans, which is still a lot but is a lot less than most dental graduates.

Knowing what we know now, she would have attended a school much closer to home and saved more money. But, that was a lesson learned.

Our other debts were accumulated from making bad decisions on a few purchases. We purchased two cars that were $116,000 combined and never should have done it while being in so much debt. But, we were focused on moving to electric cars and loved the Tesla Model 3.

Looking back on it now, we would have bought cheaper cars. But, we buckled down and paid the cars off in 2 years instead of the 5 years we signed up for. Now, we own our cars and will only buy cars in cash in the future.

When Alexis was in dental school, we both did a lot of traveling to see each other. Having a long-distance relationship wasn’t easy so we put trips on our credit cards instead of saving up the cash. This was not smart and we ended up with $10,000 of credit card debt.

The bulk of our debt consisted of things we paid for that could have waited or we could have found other ways to do.

It also didn’t help that the people around us and, in our lives, had debt as well so the conversation to become debt-free never happened. Now, we have normalized the conversation of being debt-free and building wealth with our friends and family.

We grew up in low to middle-income families and money was not a common topic for us as kids. It can be a disadvantage for sure but we decided we had to take responsibility to learn everything we could as we got older.

This decision is what helped us pay off debt so fast. Let’s discuss our best tips to get out of debt and still enjoy life.

How We Paid Off Debt So Fast

I strongly believe every person should learn as much information about money as possible and take what information works best for their situation. Personal finance is personal and there’s not a one-size-fits-all solution.

Us learning from different people, allowed us to create a blueprint that helped us pay off the debt in a short period of time and help teach others to not make the same mistakes through our blog.

We started living with a purpose and being intentional with our money. This was a huge reason why getting out of debt is so important to us because it allows us to view the bigger picture and set goals for what we want to do with our money.

We Agreed to Handle Money Together and The Right Way

The day we realized we had a huge debt issue we were planning a big wedding at the same time. And as everyone knows weddings can be very expensive. For years we planned on having a big wedding with all of our friends and family there to celebrate.

We changed our minds the day we got focused on paying off debt.

It was not an easy decision but we knew it was the best decision in the long run. So, we took a trip to the courthouse and got married. We ended up saving $25,000 by not having a big wedding and instead took a trip to Punta Cana for our honeymoon which was much less than a big wedding.

In fact, we believe this decision kickstarted our debt-free journey and brought us closer together. We started making all of our financial decisions together and combined all of our money. This helped us start being on the same page with our money and it eliminated money arguments.

We strongly believe in married couples combining money because it shows unity and builds a strong bond when you are building something together. On the other hand, many people are successful with separate accounts but for us, it worked best to combine money.

We have 4 bank accounts and this has changed everything for us when it comes to money management.

Our 4 accounts are:

Joint checking account where all of our earned income is deposited.

Joint saving accounts where we deposit money each month to consistently save.

Neiko personal checking account.

Alexis personal checking account.

The reason we have 4 accounts is to have a little financial independence and enjoy money separately. Each of us gets $200 a month to spend however we like and the other person has no say-so over what the other person does with their money. We plan to adjust this amount as necessary. The most important part of this tip is that both people must agree on the amount for each personal account.

This allows us both to be able to do things we enjoy that the other person may not enjoy as much. It works great for us and the day we started this approach, we haven’t argued about money since.

Money arguments are the leading cause of divorce so this tip has allowed us to focus on our marriage and building wealth.

We Got On a Detailed Budget and Started an Emergency Fund

Shortly after marriage, we started taking budgeting more seriously. We started giving every dollar we earned a specific task. At the end of each month, we sit down together and review our money and plan for the next month.

We set a recurring calendar reminder in our phones for our monthly financial planning meeting. This holds both of us accountable to take action with our budget and reconcile our spending. This allows us to be on the same page with our plans for the next month and review spending categories where we may need to make adjustments.

Those adjustments may be removing or adding a category and increasing or decreasing the amount of money allocated to a category.

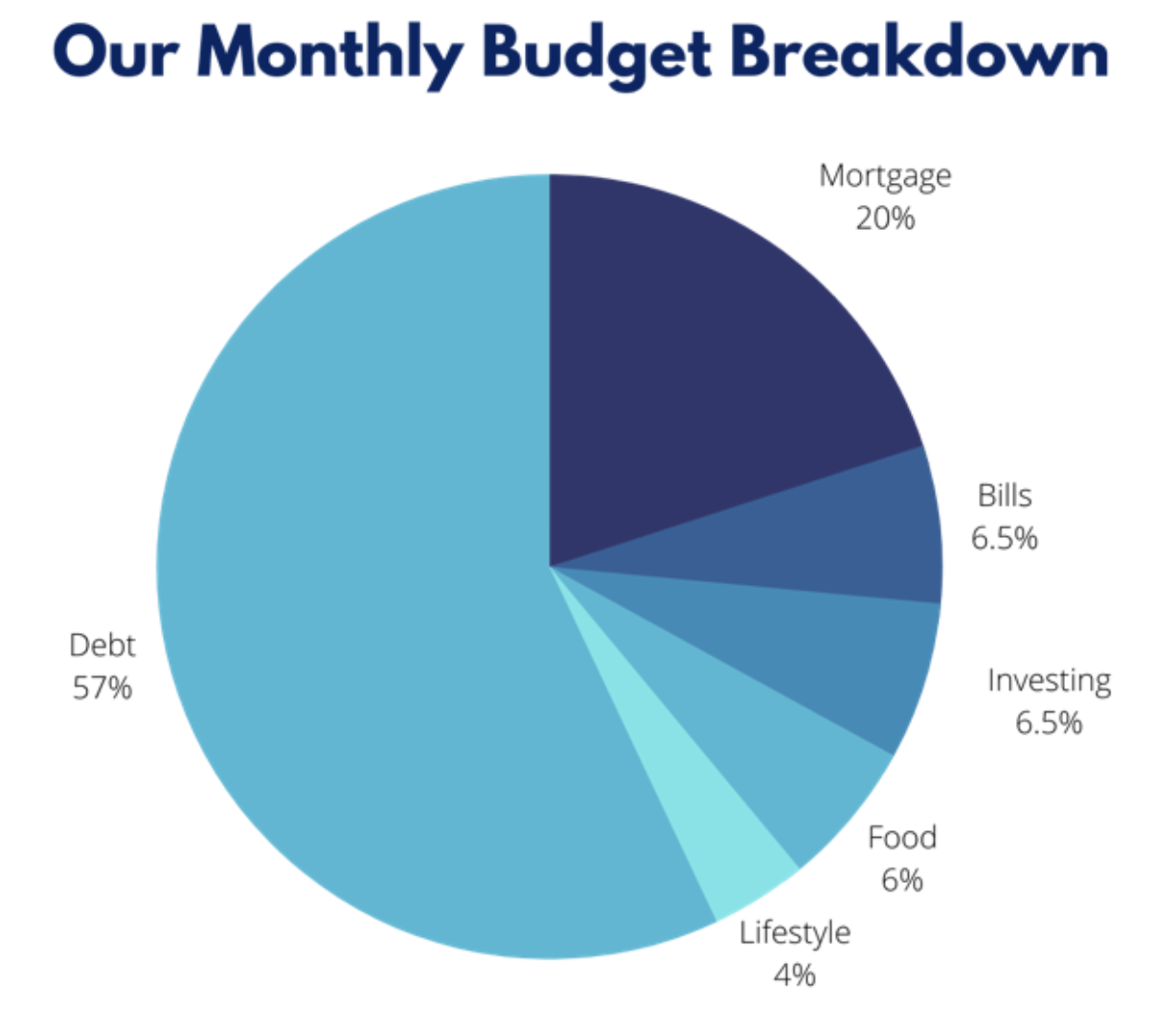

Getting on a detailed budget was important for us to be able to build an emergency fund and have some financial security when an unexpected life event happens.

Here’s a breakdown of our budget by percentages and shows how we keep our expenses low to put the extra towards debt.

Our rule of thumb is to have 1-3 months of expenses saved for an emergency while paying off debt and 3-6 months when debt-free. This is because the extra money can be used for debt until you are debt-free. The range of months all depends on your comfort level.

Some people have more secure jobs and may be comfortable having a smaller emergency fund but others may want more because their job isn’t as secure.

An emergency fund is so important regardless of your situation because you don’t want an emergency to delay you from reaching your financial goals.

We Used The Debt Snowball and Paid Extra to Debt

This method was the best for us because we wanted to keep adding more money to debt so we could pay it off faster. In fact, this is how we were able to stay on track and keep throwing extra money at our debt.

If you’ve never heard of the Debt Snowball, it’s basically where you pay your debts smallest to largest regardless of the interest rate. It’s designed to keep you motivated as you pay off one debt because you take the old payment and add it to the next largest debt.

This is why it’s called a snowball. You are building momentum to keep paying debt until it’s completely gone.

The Debt Snowball simplified our approach to debt and it was very easy for us to follow. We recommend you try it out to see if you have the same results.

We Increased Our Income and Started Side Hustles

After deciding how we would attack our debts, we also figured out we needed to increase our income to pay towards our payments.

We worked all of the extra hours we could at work and got bonuses for exceptional performance. We decided to take advantage of overtime temporarily so we can reach our financial goal faster.

Extra hours at work played a huge role in how much money we could throw at debt. Some months we were able to pay an extra $7,000 towards debt!

It was not easy to make this much extra money but we were so focused on finding extra income that we would do whatever it took to get the job done.

By starting our blog Secret to Finance, we were able to add another stream of income. It took us time to get started due to fear but we finally made the leap in March 2020 and have loved every minute. We get to tell our story about our financial journey and help others learn how to build wealth. It’s a win-win!

Starting side hustles were introduced to us from Michelle. Reading her blogs about side hustles and affiliate marketing made us more interested in blogging. It has become part of our daily lives and we think everyone should have some type of side hustle.

Entrepreneurship isn’t for everyone but there’s a side hustle out there that you can take advantage of. We even took focus groups and online surveys during our free time. Some sites paid us up to $250 for just an hour of our time! Most of the time we completed these focus groups on our lunch break and it didn’t require much effort.

Starting a side hustle is all about being creative and finding ways to increase income to speed up your debt-free journey.

Our Best Tips For Other People To Pay Off Debt Fast and Reach Financial Goals

When it comes to money management and building wealth you should always do what works best for you and your family. Everyone has a different situation and it’s so important to focus on things you value and care about.

You work hard for your money and you should focus on spending your money wisely. Other people will always try to convince you to do something that you may not be 100% comfortable with. It’s so key to only spend money on things you understand.

Go slow and take your time to make sure you understand what you’re doing with your finances.

It’s not a problem to be unsure about how to do something. But, it’s even more important to take time to educate yourself and make the best decision for you.

Getting out of debt and building wealth can be hard and frustrating. But, once you figure out a plan that works for you, go all-in on that plan and you will be on your way to building wealth.

Our approach to money management is:

Handling money the right way

Get on a detailed budget

Build an emergency fund

Get out of debt using the debt snowball method and pay extra towards debt

Increase income

Start a side hustle

Do you have debt? What are you doing to pay off your debt?

The post How (And Why) We Paid Off $240,000 Of Debt In 27 Months appeared first on Making Sense Of Cents.

Article Source and Credit makingsenseofcents.com https://www.makingsenseofcents.com/2021/07/how-and-why-we-paid-off-240000-of-debt-in-27-months.html Buy Tickets for every event – Sports, Concerts, Festivals and more buytickets.com

Leave a Reply

You must be logged in to post a comment.